Random Forests

- Bagging can turn a single tree model with high variance and poor predictive power into a fairly accurate prediction function.

- But bagging suffers from tree correlation, which reduces the overall performance of the model.

- Random forests are a modification of bagging that builds a large collection of de-correlated trees

- It is a very popular out-of-the-box learning algorithm that enjoys good predictive performance.

Extending the bagging technique

- Bagging introduces a random component in to the tree building process

- The trees in bagging are not completely independent of each other since all the original predictors are considered at every split of every tree.

- Trees from different bootstrap samples have similar structure to each other (especially at the top of the tree) due to underlying relationships.

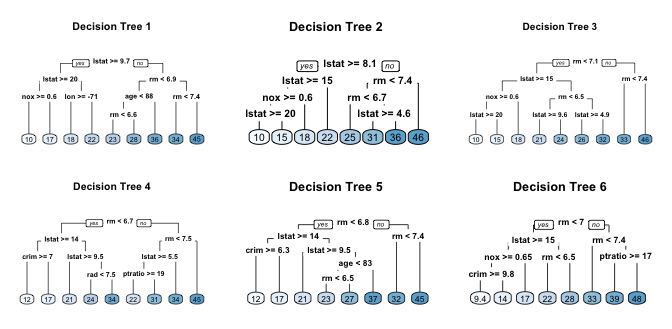

Similar trees - tree correlation

- If we create six decision trees with different bootstrapped samples of the Boston housing data, the top of the trees all have a very similar structure.

- Although there are 15 predictor variables to split on, all six trees have both

lstatandrmvariables driving the first few splits.

Tree correlation

- Tree correlation prevents bagging from optimally reducing variance of the predictive values.

- To reduce variance further, we need to minimize the amount of correlation between the trees.

- This can be achieved by injecting more randomness into the tree-growing process.

Random forests achieve this in two ways:

1) Bootstrap:

- Similar to bagging, each tree is grown to a bootstrap resampled data set, which makes them different and decorrelates them.

2) Split-variable randomization:

- For every split, the search for the split variable is limited to a random subset of $m$ of the $p$ variables.

- For regression trees, typical default values are $m=p/3$ (tuning parameter).

- When $m=p$, the randomization is limited (only step 1) and is the same as bagging.

Basic algorithm

The basic algorithm for a regression random forest can be generalized:

1. Given training data set

2. Select number of trees to build (ntrees)

3. for i = 1 to ntrees do

4. | Generate a bootstrap sample of the original data

5. | Grow a regression tree to the bootstrapped data

6. | for each split do

7. | | Select m variables at random from all p variables

8. | | Pick the best variable/split-point among the m

9. | | Split the node into two child nodes

10. | end

11. | Use tree model stopping criteria to determine: tree complete

12. end

The algorithm randomly selects a bootstrap sample to train and predictors to use at each split.

Characteristics

- Since bootstrap samples and features are selected randomly at each split, we create a more diverse set of trees, which tends to lessen tree correlation beyond bagged trees and often dramatically increase predictive power. <!–

- random forests have the least variability in their prediction accuracy when tuning. –>

out-of-bag error

- Similar to bagging, a natural benefit of the bootstrap resampling process is that random forests have an out-of-bag (OOB) sample that provides an efficient and reasonable approximation of the test error.

- This provides a built-in validation set without any extra work, and you do not need to sacrifice any of your training data to use for validation.

- We are more efficient identifying the number of trees required to stablize the error rate <!– during tuning;

Out-of-bag error vs. validation error

- Some difference between the OOB error and test error are expected.

–>

–>

Preparation - random forests

- The following slides are based on UC Business Analytics R Programming Guide on random forests

library(rsample) # data splitting

library(randomForest) # basic implementation

library(ranger) # a faster implementation of randomForest

# an aggregator package for performing many

# machine learning models

library(caret)

The Ames housing data

set.seed(123)

ames_data <- AmesHousing::ames_raw

set.seed(123)

ames_split <- rsample::initial_split(ames_data,prop=.7)

ames_train <- rsample::training(ames_split)

ames_test <- rsample::testing(ames_split)

Basic implementation

- There are over 20 random forest packages in R.

- To demonstrate the basic implementation we use the

randomForestpackage, the oldest and most well known implementation of the random forest algorithm in R. - As your data set grows in size

randomForestdoes not scale well (although you can parallelize withforeach). - To explore and compare a variety of tuning parameters we can find more effective packages.

- The package

rangerwill be presented in the tuning section.

randomForest::randomForest

randomForestcan use the formula or x-y matrix notation.- Below we apply the default

randomForestmodel using the formal specification. - The default random forest performs 500 trees and $\dfrac{\text{nr. features}}{3}=26$ randomly selected predictor variables at each split.

set.seed(123)

# default RF model

(m1 <- randomForest(formula = Sale_Price ~ .,data=ames_train))

##

## Call:

## randomForest(formula = Sale_Price ~ ., data = ames_train)

## Type of random forest: regression

## Number of trees: 500

## No. of variables tried at each split: 26

##

## Mean of squared residuals: 639516350

## % Var explained: 89.7

Plotting the model

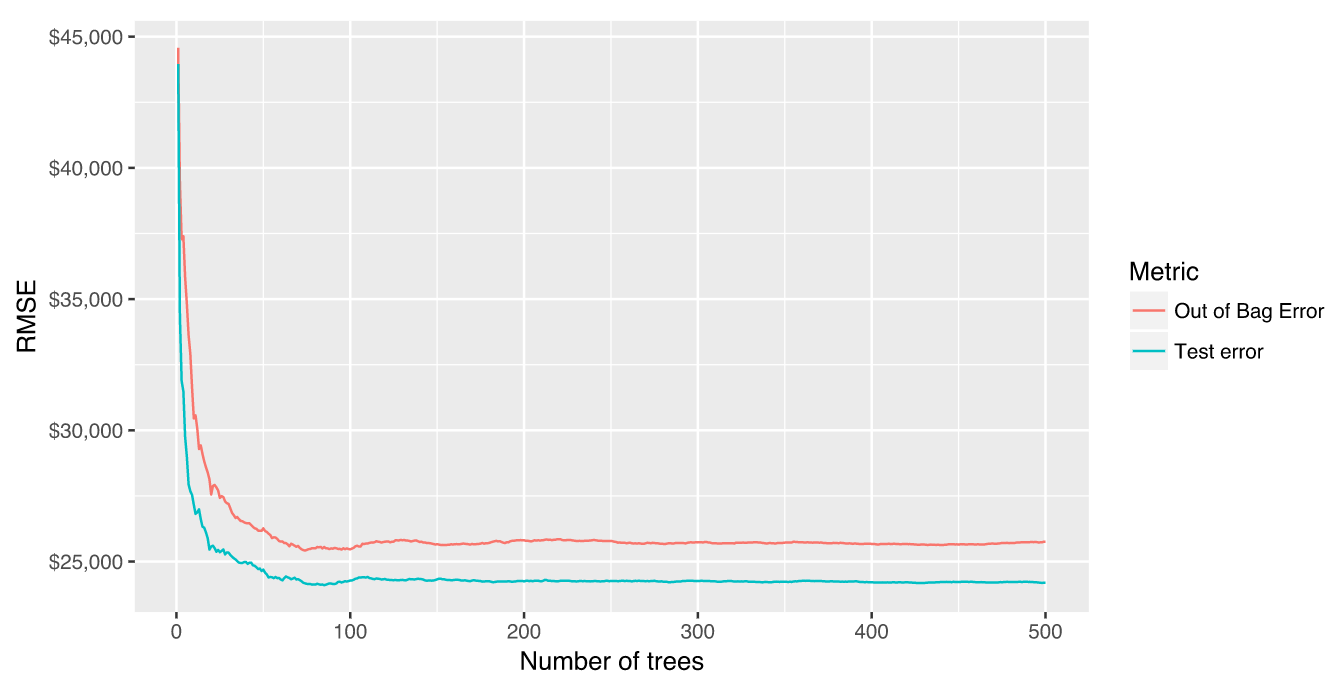

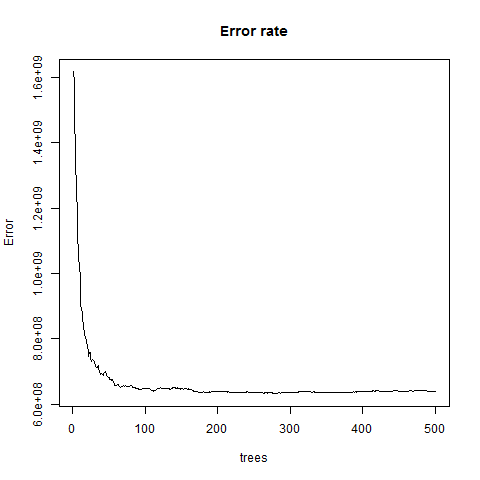

- The error rate stabalizes with around 100 trees but continues to decrease slowly until around 300 trees.

plot(m1,main="Error rate")

{height=65%}

{height=65%}

Random forests - out-of-the-box algorithm

- Random forests perform remarkably well with very little tuning.

- We get an RMSE of less than 30K dollar without any tuning.

- This is more than 6K dollar RMSE-reduction compared to a fully-tuned bagging model

- and 4K dollar reduction to to a fully-tuned elastic net model.

- We can still seek improvement by tuning our random forest model.

Tuning Random forests

- Random forests are fairly easy to tune since there are only a handful of tuning parameters.

- First we tune the number of candidate variables to select from at each split.

- A few additional hyperparameters are important.

Tuning parameters (I)

- The following hyperparameter are important (names may differ across packages):

number of trees

ntree- We want enough trees to stabalize the error but using too many trees is inefficient, esp. for large data sets.

number of variables

mtry- number of variables as candidates at each split. Whenmtry=pthe model equates to bagging.- When

mtry=1the split variable is completely random, all variables get a chance but can lead to biased results. Suggestion: start with 5 values evenly spaced across the range from 2 to p.

Tuning parameters (II)

Number of samples

sampsize- Default value is 63.25% since this is the expected value of unique observations in the bootstrap sample.- Lower sample sizes can reduce training time but may introduce more bias. Increasing sample size can increase performance but at risk of overfitting - it introduces more variance. <!–

- When tuning this parameter we stay near the 60-80% range. –>

Tuning parameters (III)

minimum number of samples within the terminal nodes:

nodesize- Controls the complexity of the trees.- It is the minimum size of terminal nodes.

- Smaller node size allow for deeper, more complex trees

- This is another bias-variance tradeoff where deeper trees introduce more variance (risk of overfitting)

- Shallower trees introduce more bias (risk of not fully capturing unique patters and relatonships in the data).

maximum number of terminal nodes

maxnodes: A way to control the complexity of the trees.- More nodes equates to deeper, more complex trees.

- Less nodes result in shallower trees.

Initial tuning with randomForest

- If we just tune the

mtryparameter we can userandomForest::tuneRFfor a quick and easy tuning assessment. <!– tuneRfwill start at a value ofmtrythat you supply and increase by a certain step factor until the OOB error stops improving. –>- We start with 5 candidate variables (

mtryStart=5) and increase by a factor of 2 until the OOB error stops improving by 1 per cent. tuneRFrequires a separate x y specification.- The optimal

mtryvalue in this sequence is very close to the default mtry value of $\dfrac{\text{features}}{3}=26$.

features <- setdiff(names(ames_train), "Sale_Price")

set.seed(123)

m2<-tuneRF(x= ames_train[,features],

y= ames_train$Sale_Price,ntreeTry = 500,

mtryStart = 5,stepFactor = 2,

improve = 0.01,trace=FALSE)

Full grid search with ranger

- To perform a larger grid search across several hyperparameters we’ll need to create a grid, loop through each hyperparameter combination and evaluate the model.

- Unfortunately, this is where

randomForestbecomes quite inefficient since it does not scale well. - Instead, we can use

rangerwhich is a C++ implementation of Breiman’s random forest algorithm and is over 6 times faster thanrandomForest.

Assessing the speed

randomForest speed

system.time(

ames_randomForest <- randomForest(

formula = Sale_Price ~ .,

data = ames_train,

ntree = 500,

mtry = floor(length(features) / 3)

)

)

# User System elapsed

# 145.47 0.09 152.48

ranger speed

system.time(

ames_ranger <- ranger(formula=Sale_Price ~ .,

data = ames_train,num.trees = 500,

mtry = floor(length(features) / 3))

)

## user system elapsed

## 9.13 0.03 3.23

The grid search

- To perform the grid search, we construct our grid of hyperparameters.

# hyperparameter grid search

hyper_grid <- expand.grid(

mtry = seq(20, 30, by = 2),

node_size = seq(3, 9, by = 2),

sampe_size = c(.55, .632, .70, .80),

OOB_RMSE = 0

)

- We search across 96 different models with varying

mtry, minimum node size, and sample size.

nrow(hyper_grid) # total number of combinations

## [1] 96

Loop - hyperparameter combination (I)

- We apply 500 trees since our previous example illustrated that 500 was plenty to achieve a stable error rate.

- We set the random number generator seed. This allows us to consistently sample the same observations for each sample size and make the impact of each change clearer.

for(i in 1:nrow(hyper_grid)) {

model <- ranger(formula= Sale_Price ~ .,data= ames_train,

num.trees = 500,mtry= hyper_grid$mtry[i],

min.node.size = hyper_grid$node_size[i],

sample.fraction = hyper_grid$sampe_size[i],

seed = 123)

# add OOB error to grid

hyper_grid$OOB_RMSE[i] <- sqrt(model$prediction.error)

}

The results - samll difference between RMSE

hyper_grid %>% dplyr::arrange(OOB_RMSE) %>% head(10)

## mtry node_size sampe_size OOB_RMSE

## 1 26 3 0.8 25404.60

## 2 28 3 0.8 25405.92

## 3 28 5 0.8 25459.46

## 4 26 5 0.8 25493.80

## 5 30 3 0.8 25528.26

## 6 22 3 0.7 25552.73

## 7 26 9 0.8 25554.31

## 8 28 7 0.8 25578.45

## 9 20 3 0.8 25581.23

## 10 24 3 0.8 25590.73

- Models with slighly larger sample sizes (70-80 per cent) and deeper trees (3-5 observations in terminal node) perform best.

- We get various

mtryvalues in top 10 - not over influential.

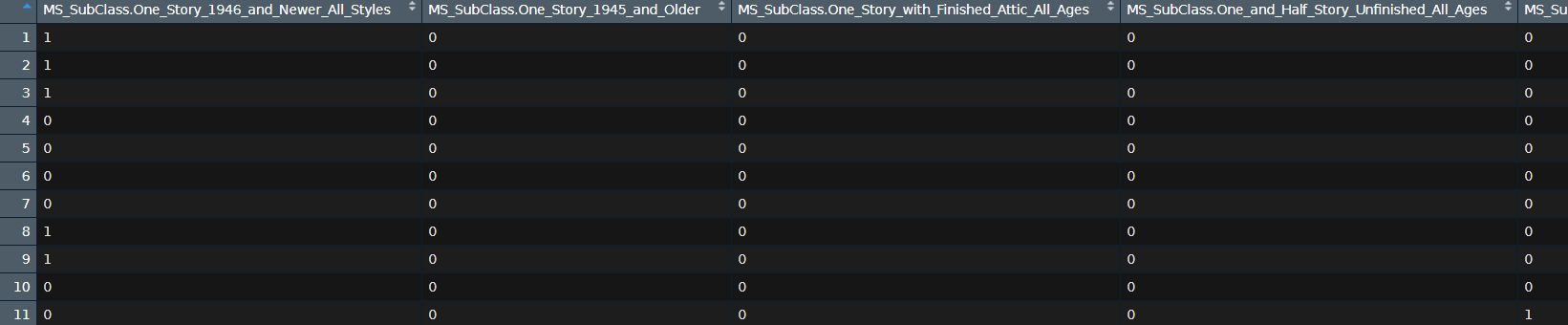

Hyperparameter grid search - categorical variables

- We use one-hot encoding for our categorical variables which produces 353 predictor variables versus the 80 we were using above.

# one-hot encode our categorical variables

(one_hot <- dummyVars(~ ., ames_train, fullRank = FALSE))

## Dummy Variable Object

##

## Formula: ~.

## 81 variables, 46 factors

## Variables and levels will be separated by '.'

## A less than full rank encoding is used

Make a dataframe of dummy variable object

ames_train_hot<-predict(one_hot,ames_train)%>%as.data.frame()

Hot encoding and hypergrid

# make ranger compatible names

names(ames_train_hot) <- make.names(names(ames_train_hot),

allow_ = FALSE)

# --> same as above but with increased mtry values

hyper_grid_2 <- expand.grid(

mtry = seq(50, 200, by = 25),

node_size = seq(3, 9, by = 2),

sampe_size = c(.55, .632, .70, .80),

OOB_RMSE = 0

)

The best model

The best random forest model:

- uses columnar categorical variables

mtry= 24,- terminal node size of 5 observations

- sample size of 80%.

How to proceed

- Repeat the model to get a better expectation of error rate.

Random forests with ranger

- The

impuritymeasure is the variance of the responses for regression impurityis a measure for heterogeneity - it measures how well the classes are

<!– https://stats.stackexchange.com/questions/220321/what-is-node-impurity-purity-in-decision-trees-in-plain-english-why-do-we-need

https://people.cs.pitt.edu/~milos/courses/cs2750-Spring03/lectures/class19.pdf –>

OOB_RMSE <- vector(mode = "numeric", length = 100)

for(i in seq_along(OOB_RMSE)) {

optimal_ranger <- ranger(formula= Sale_Price ~ .,

data = ames_train,

num.trees = 500,

mtry = 24,

min.node.size = 5,

sample.fraction = .8,

importance = 'impurity')

OOB_RMSE[i] <- sqrt(optimal_ranger$prediction.error)

}

Variable importance / node impurity

- Node impurity represents how well the trees split the data. There are several impurity measures;

-

Gini index, Entropy and misclassification error are options to measure the node impurity

- We set

importance = 'impurity', which allows us to assess variable importance. - Variable importance is measured by recording the decrease in MSE each time a variable is used as a node split in a tree.

- The remaining error left in predictive accuracy after a node split is known as node impurity. <!– https://medium.com/the-artificial-impostor/feature-importance-measures-for-tree-models-part-i-47f187c1a2c3 http://www.cse.msu.edu/~cse802/DecisionTrees.pdf https://www.cs.indiana.edu/~predrag/classes/2017fallb365/ch4.pdf

http://mason.gmu.edu/~jgentle/csi772/16s/L10_CART_16s.pdf

https://stats.stackexchange.com/questions/158583/what-does-node-size-refer-to-in-the-random-forest –>

- A variable that reduces this impurity is considered more imporant than those variables that do not.

- We accumulate the reduction in MSE for each variable across all the trees and the variable with the greatest accumulated impact is considered the more important.

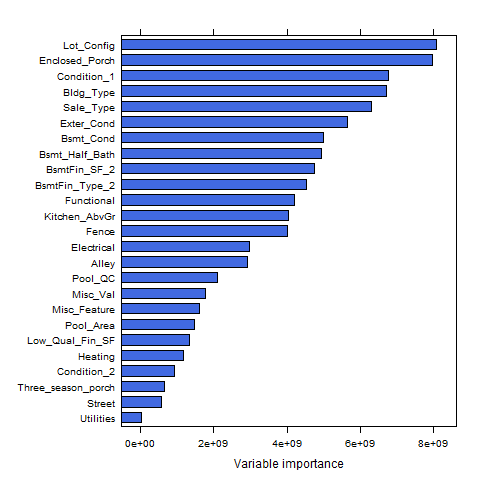

Plot the variable importance

varimp_ranger <- optimal_ranger$variable.importance

lattice::barchart(sort(varimp_ranger)[1:25],col="royalblue")

- We see that Utilities has the greatest impact in reducing MSE across our trees, followed by

names(sort(varimp_ranger))[2], Low_Qual_Fin_SF, etc.

{height=60%}

{height=60%}

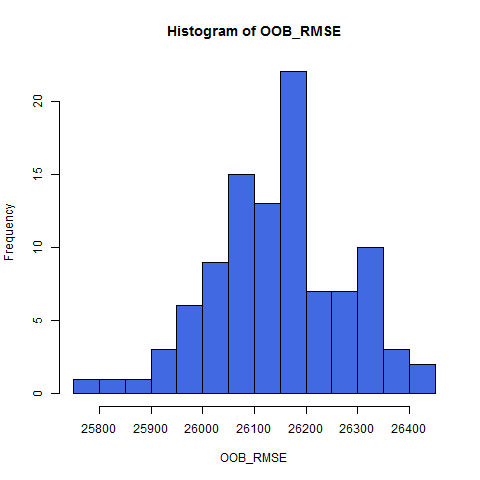

A histogram of OOB RMSE

hist(OOB_RMSE, breaks = 20,col="royalblue")

{height=75%}

{height=75%}

Predicting

- With the preferred model we can use the traditional predict function to make predictions on a new data set.

- We can use this for all our model types (

randomForestandranger); although the outputs differ slightly. <!– - not that the new data for the

h2omodel needs to be anh2oobject. –>

# randomForest

pred_randomForest <- predict(ames_randomForest, ames_test)

head(pred_randomForest)

## 1 2 3 4 5 6

## 113543.1 185556.4 259258.1 190943.9 179071.0 480952.3

# ranger

pred_ranger <- predict(ames_ranger, ames_test)

head(pred_ranger$predictions)

## [1] 129258.1 186520.7 265628.2 197745.5 175517.6 392691.7

Summary - random forests

- Random forests provide a very powerful out-of-the-box algorithm that often has great predictive accuracy.

- Because of their more simplistic tuning nature and the fact that they require very little, if any, feature pre-processing they are often one of the first go-to algorithms when facing a predictive modeling problem.

Advantages & Disadvantages

Advantages - random forrests

- Typically have very good performance

- Remarkably good “out-of-the box” - very little tuning required

- Built-in validation set - don’t need to sacrifice data for extra validation

- No pre-processing required

- Robust to outliers

Disadvantages - random forrests

- Can become slow on large data sets

- Although accurate, often cannot compete with advanced boosting algorithms

- Less interpretable

Links

These slides are mainly based on

-

A UC Business Analytics R Programming Guide - section random forests

-

and on the chapter on random forests in the e-book of Brad Boehmke and Brandon Greenwell - Hands-on Machine Learning with R